Stock returns are skewed, but how much is shocking

- Jul 28, 2024

- 2 min read

The difference between the median and the average cumulative returns of US stocks since 1926 is amazing...

Reminder: Median is the middle of a range of values (in this case stock returns); 50% of all values are above the median, and 50% of the values are below the median. Average is the sum of all values (returns) divided by the number of observations (in this case number of stocks). Median is usually considered as a “cleaner” statistical parameter than average (because the average can be heavily skewed by a few outliers).

As mentioned by @SpencerHakimian on X: "Stock returns are so skewed to the 4% of stocks that are responsible for all equity market returns that have occurred in the past 100 years.

Statistically, it is virtually impossible to outperform an index over time since you would have needed to specifically own the tiny percentage of stocks that beat the index, and specifically avoid the vast majority of stocks that underperformed the index.

Individual stock picking turns investing from a positive sum game to a negative sum game. Index investing is like being the casino. Individual stock picking is like being the gambler".

Another picture to show that skewness is below.

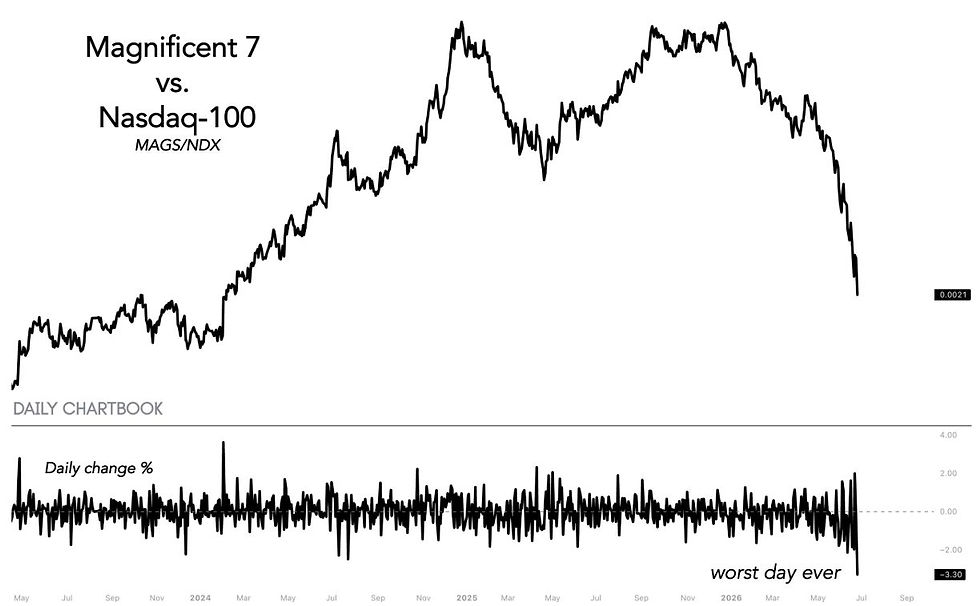

And then to amplify with an example: how big the Magnificent 7 (Alphabet (Google), Amazon, Apple, Meta Platforms (Facebook), Microsoft, NVIDIA and Tesla) has become!

The Magnificent 7's market cap is higher than any non-US stock market in the world. The group is worth now ~$15.7 trillion, almost double China’s stock market value of $8.7 trillion. It is also worth nearly as much as the German, Canadian, UK, French, and Indian stock markets COMBINED. Apple, Nvidia, and Microsoft each are worth more than the German and Canadian markets. To put this into another perspective, the total US stock market is worth $50 trillion, just 3 times more than the Magnificent 7.

Sources: Baird, Michel A.Arouet, Hendrik Bessembinder, hiddenaluegems, kobeissiletter, Bloomberg

Comments